Because There Can Be More To The Good Life, A Higher Level, A More Abundant Life -

From Mere Wealth To Prosperity

Wealth preserving economic insights make living the best of the good life prudent wealth management

|  |  |

|---|---|---|

|

Can YES help You Ensure Success? See for yourself.

How do you define success? By almost any measure - there is at least some economic component.

For many, success is financial achievement. For some economic rewards result from a job well done. Others, believe they're financially blessed to bless others, measure success by the "good" they achieve.

Thus, by almost any measure, YES can help you ensure success. We invite you to "sea" for yourself.

Why are we now willing to walk non clients through some of the best kept secrets of the super rich?

Aside from the obvious economic possibilities, let's just call it the law of the sea, a duty to rescue.

As we explain in Lower Taxes? YES Your Expected Savings- most can now cut their taxes by 50% & more.

Because of the recent sea change in the U S tax code, from The Tax Cuts And Jobs Act (TCJA) to the Biden tax plans, many need to replace their outdated tax planning strategies. Higher tax rates, new taxes, with most of the previously allowed and encouraged deductions are to be substantially reduced, restricted or repealed entirely.

As a result, most of the best tax plans that kept the effective top rates around 26 - 28% for those with AGI over $500k are now dashed wrecks on the rocks - or at least taking on water and sinking fast.

With YES, tax payers can expect effective maximum rates of only 9.6 – 19%. Now that we can help lower taxes by 50% and more, how can we in good conscience not try to help as many people as possible? Especially those highly compensated W2 employees - and particularly those in high tax states.

Tax Cuts Benefit the Ultra Rich,

but Not the Merely Rich

Many on Wall Street and in corporate America are scrambling to understand how much bigger their bill will be.

-

Dec. 18, 2017

Here’s the nuance: The tax bill soaks some of rich Americans — but it does not soak the richest.

It is the “pretty rich” right below that level that may get hit: the W2 employee making several hundred thousand dollars to millions of dollars a year with high state and local taxes that will not be fully deductible may see a higher tax bill. So will the chief executives of many large publicly traded companies who often itemize large, unreimbursed business expenses, which will no longer be allowed. Some executives are already calculating that they will be paying additional seven-figure sums in taxes.

Let's see how the wealth building secrets of George Soros and the super rich can work for you.

STEP I

A good place to start is to find out based upon your Adjusted Gross Income, your estimated taxes and then your estimated tax savings.

Below, are embedded two calculators from independent third party websites to assure against any mistakes, or self serving manipulations. One is a tax calculator and the other an investment calculator.

There are many such calculators available, and please feel free to use your own. We simply chose to provide these embeds for your convenience, but links are also provided if you prefer.

In the embedded tax calculator below, simply scroll down the Smart Asset window and provide 3 items: Household Income, Location and Filing Status. It will provide estimates of not just your federal taxes but state and local as well as FICA.

Then it provides what it refers to as "Trump Taxes" to show the effect of the TCJA in 2018 and beyond.

For example a single tax payer earning $1,000,000 in New York, NY will pay more in total taxes from $453,000 to $465,000. In Miami Beach, FL, Trump Taxes cut taxes from $378,000 to $360,000.

After estimating your tax from the calculator - cut it in half - or look at the chart below. This will show how much immediate tax savings will be available for other more productive uses - such as investing.

For example, if the tax calculator estimates taxes of $200,000, for discussion purposes going forward, assume that YES can in fact reduce taxes for most by at least 50%. Thus your estimated tax going forward should be only $100,000 with $100,000 in tax savings now available for other investments.

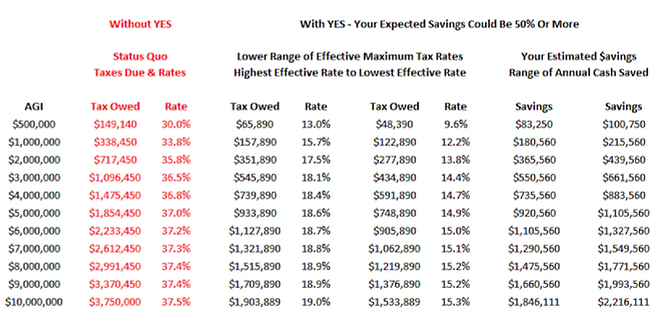

Or use the generic chart below with the most conservative worst case scenarios, to compare what a range of hypothetical tax payers could expect to pay - both in tax rates and dollar expenditures. Under the current status quo without YES - versus the maximum taxes they could expect to pay with YES.

Federal Tax Estimate: Single, No dependents, W2 ordinary income as only source of Adjusted Gross Income (AGI)

In order to keep things simple for educational purposes only, assume highly compensated W2 employees such as a professional athletes, physicians, corporate executives, entertainers, entrepreneurs, etc.

All tax payers are single, with no dependents and Adjusted Gross Income (AGI) is only W2 employee ordinary salary income ranging from $500,000 to $10,000,000.

Keep in mind, this should be the maximum tax.

There is simply no longer any reason to pay more than 20% in federal taxes – even as a highly compensated W2 employee - unless you wish to or don't know any better.

In fact, the actual savings and benefits could - and should- be substantially greater with the appropriate planning tailored to the individual tax payer; their situation, goals and resources.

For example, a married taxpayer filing jointly with no dependents and with $750,000 of AGI of only salary income- if he does nothing- could owe about $212,000 in federal taxes.

However, by combining several of the most frequently overlooked tax code provisions along with our basic strategies, it would be relatively easy to reduce his federal tax liability on ordinary income of $750,000 to a range of between $13,000 – $19,000.

Simply put - a tax savings of about a $200,000 is possible or $20,000 tax on $750,000 of income. But any such personal tax planning is beyond the immediate scope.

STEP II

Whatever amount is saved in taxes - is then prudently invested.

This basic Future Value Calculator is adequate for our purposes and perhaps more importantly is convenient with only 4 inputs.

Number of Periods is the number of years we want for the investment. For 5 years enter 5.

Starting amount is the initial amount invested - or for our purposes - the tax savings.

Interest rate is the expected investment yield.

As for the variable Periodic Deposit (PMT) $ / period - simply enter 0 to start since we want to calculate just the future value of the initial tax savings.

For example, a single investment of $100,000 at 12% with no other money invested grows to over $176,000 over 5 years. A $1,000,000 tax savings invested at 15% more than doubles in 5 years.

Next, consider that if YES shows you how to save $100,000 in taxes, it's logical that you would continue with the same strategy as long as you have the income and the strategy would provide the same tax savings under the code. It is highly unlikely you would revert to the old way and over pay your taxes by more than twice as much as necessary.

Thus, now add the same dollar amount of tax savings to the last variable to show an additional deposit of the same tax savings in in each of the next few years. In this example it would be $100,000, but your actual number will vary depending on your calculated tax savings.

So in this example of a tax savings of $100,000 each year for 5 years that could be invested at 12% would grow to over $800,000 after only the first 5 years.

Consequently, we are not just looking at a $100,000 first year tax savings, but really much more.

Depending on the timing, something approaching a 5 year value close to 9 - 10 times the actual first year estimated tax savings depending on the length of the investment period and the average investment yields over the period could be expected.

This is especially noteworthy considering the uncertainty and unpredictability of most sports and entertainment careers.

One day you're "HOT", the next you're "HISTORY". Many professional athletes are W2 employees, almost 80% are insolvent within 5 years of "retirement", with relatively brief average professional athlete careers:

-

NFL: 3.5 years

-

NBA: 4.8 years

-

MLB: 5.6 years

-

NHL: 5.5 years

|

|---|

|

|

|

|

As explored elsewhere in more detail:

For example, assume a tax payer is able to reduce their taxes by $1,000,000 this year. He then invests that $1,000,000 for 5 years at an Internal Rate of Return (IRR) of only 10% so that at the end of 5 years it would be about $1.6 million. Or if he is a business owner, perhaps he can generate a much higher return on his investment for a longer period - lets say 20% for 10 years - then his initial tax savings would be worth about $6.2 million.

So how much did this tax payer actually save?

As a result of these new tax strategies that reduced his taxes, how much did his net worth increase or would be available to his heirs? Is it only $1,000,000 or is it $1,600,000 or maybe $6,200,000?

Then you have to keep in mind that this is probably not a single year tax savings but a multi-year program. So lets say our tax payer is now able to reduce his taxes by $1,000,000 each year for 10 years and is able to invest the tax savings at 20% for 10 years.

Did this tax payer save only $1,000,000 - just what he saved in the first year?

Or did he actually save - and increase his net worth - by $62,000,000 - by what he was able to save each year for 10 years and then accumulate by successfully investing those tax savings into more productive alternatives?

So what do you think?

How much can your net worth increase if we cut your taxes by 50% and invest the savings?

Or, what is your opportunity cost?

How much is it really costing you if you don't cut your taxes by 50% and invest the savings?

STEP I - STOP OVER PAYING YOUR TAXES

STEP II - INVEST YOUR TAX SAVINGS WISELY

It worked for George Soros. It works for others. No reason we can't make it work for you.

Recent research reveals that one's tax rate can have up to 10 times greater influence over long term wealth accumulation then one's actual asset allocation or investment portfolio. Up to 10 times more impact on one's wealth, and it goes largely ignored - or accepted - by the most affluent.

Per Bloomberg, a hedge fund manager with Soros' record starting with $12 million, and not taking any more investor money, and reinvesting his share of the profits pretax, would have after 40 years

$15.9 Billion.

Had taxes been paid at the time the income was earned, the original $12 million investment would have grown to only

$2.4 Billion.

With available tax deferral strategies, Soros' net worth was at the time of the story around

$28.8 Billion

C.World Economic Forum, CC BY-SA 2.0, via Wikimedia Commons

A brief word about what to do with your tax savings.

We are NOT investment advisors. We are not financial planners. We do not sell insurance or provide any other estate planning product or service. We do not offer any type of investment or securities for sale or express any opinions or provide advice concerning such.

Nevertheless, our unique skill set can provide unique economic insights and advantages.

We know how to make the luxury lifestyle more rewarding in both the short and long terms- while reducing risk and uncertainty.

For example, the "net worth neutral" yachting strategies that make yacht ownership profitable are applicable to other asset classes and alternative opportunities. There's no longer any reason to have any problem assets. Frequently the very types of non approved assets or investments that most advisors are neither trained nor qualified to opine upon and often prohibited from even discussing.

We know how to create a competitive information advantage that provides superior risk adjusted returns. We are especially adept at risk identification, mitigation, and more importantly properly pricing any risk premium.

We understand the difference between retail and wholesale opportunities and between wealth preservation strategies versus accumulation. We are adept with a range of perspectives, the more conservative - "clippers" that are satisfied with a 2% tax free coupon yield, the "investors" that think anything consistently above 11% is too good to be true, while the entrepreneurs don't even want to talk about yields less than 30% or higher.

All want some type and to various extents - an information advantage to mitigate any potential risk.

We serve as another set of eyes offering a different perspective to help make sure nothing falls through the cracks or is overlooked. Thus some financial advisors, for the same reasons as many CPAs, may at least initially misunderstand and feel threatened by our presence and the services we provide.

What CPAs & other advisers say is NOT always exactly what they really mean is the gist of a 1996 Patrick Rice article, "What to do when your CPA says, you can't do that".

The takeaway was that CPAs, like many professionals, often say things that can mean something different to a lay person resulting in very costly misunderstandings.

When a CPA, financial advisor, broker, etc. says, "You can't do that," whatever "that" investment or project is you are trying to do, what they really mean is: "You can't do that - here with me".

Because:

-

"I've never heard of that,

-

I don't know anything about that,

-

I don't know how to do that, or

-

I can't make any money if you do that."

Therefore, since I can't do that, then no one else can do that either.

As economic consultants, we don't replace or compete with your current CPA, legal or financial advisors, but are essential supplements thereto. We provide specialized expertise and a competitive information advantage that complements and enhances the productivity of everyone's current as well as future efforts.

Our contributions help ensure maximum efficiency and prosperity - with a special emphasis for those opportunities that might otherwise fall through the cracks or be overlooked.

In fact, the best and the brightest tax advisors, financial planners, and wealth managers should welcome our addition to the team. They recognize our unique skills can relieve some of their burdens, making their jobs easier, more productive and efficient, thereby enabling them to provide better service and greater value to even more of their clients.

As much as some may try,

no one can be an expert on everything.

Over the years we have found a few constants:

-

The higher the income, the more one tends to consistently over pay their taxes, and

-

We can usually find items that have been consistently ignored or overlooked for years by some of the the best CPAs and other advisors for that can reduce the annual taxes of high income earners between 30 - 50%.

-

It's impossible to "beat" the market when in essence you "are" the market.

-

What everybody "knows" - is seldom worth much.

-

No one knows everything.

-

Never play another man's game.

Understandably, at first impression, many may be surprised by those figures assuming that more affluent tax payers would have better outcomes since they can easily afford and they usually paid for the "best" tax advice and counsel. And in some respects that is true.

The fact that nobody knows everything is just as applicable for investing and investment advisors as it is for taxes and CPAs - if not more so.

Taxes, Yachts & Wealth Preservation

As the tax code becomes increasingly more complicated, enforcement seems more arbitrary and interpretation less predictable - yet many expect their CPA to know everything about everything.

However when it comes to investing and providing investment advice, the industry acknowledges the advisor's limitations and prevents them from advising on alternative opportunities not authorized and approved by the firm for which any particular advisor is an expert.

Let's face it. Most financial advisors and wealth managers are largely salesmen. Even if highly trained, most are compensated to convince investors to buy or invest in someone else's stock, product, or offering.

Over burdened advisors - no matter their credentials,

adversely affect your taxes, net worth, and your lifestyle.

To a great extent, few financial advisors or wealth managers have the time or expertise to perform their own due diligence and rely upon others in the firm to vet appropriate investments for them to "recommend".

Thus in many ways, investment professionals are victims of the same problems and limitations that plague accounting professionals.

There are just too many alternative opportunities both tax and investment that are "off the radar" for everyone to always be sufficiently knowledgeable.

_edited.jpg)

_edited.jpg)

_edited.jpg)

_edited.jpg)

Could your current advisors be missing something? Could another set of eyes help?

Many will not be surprised to learn they have significantly over paid their taxes for years. They have "sort of been wondering about their current tax advisors" for some time feeling they may have "outgrown" them but chose to remain out of a sense of misplaced loyalty.

Professional tax, legal, financial advisors and wealth managers have a difficult if not impossible challenge keeping abreast of all the tax and regulatory changes of their practice specialty – much less find the time and resources to focus on the potential effects of only a sub-set of their clientele with unique interests.

Likewise, many of the more financially successful and sophisticated will know of investment opportunities that many of the retail investing community may find hard to believe.

_edited.jpg)

For example, it is the very rare advisor that makes his clients' hobbies and lifestyle interest a priority - much less with the time, resources, and ability to proactively seek out and design strategies that may have little value to other clients or other industries.

Understandably your advisors must prioritize their limited resources to address the needs of the majority of their clients.

Not surprisingly, some of the lesser known, newer, or more specialized benefits and strategies may from time to time be overlooked until brought to the specific attention of your regular CPA, attorney, or financial advisor or wealth manager.

Unfortunately, too many affluent tax payers just assume there is not that much difference between qualified professionals, or that if they pay a high price for advice to a recognized name that the advice must be "good".

Many affluent tax payers simply don't know how to check the quality of their current advice and seldom get second opinions - from those that are qualified and independent to even have an educated opinion. They become comfortably complacent. That can be a costly mistake.

We are able to focus on only a select few areas and on the needs of a select clientele. Our uniquely targeted expertise and perspective; enables us to provide unsurpassed insights to help our clients and partners achieve their tax and wealth management objectives.

That if your current advisors knew, surely they'd have told you already- wouldn't they?